Pension or lump-sum payout?

When you retire, you have the choice of withdrawing your pension funds in the form of a monthly pension, a lump sum or a combination of both. Compare what is most beneficial for you.

Lump-sum vs. pension payment

Note: This calculator is based on general and simplified assumptions and provides a rough overview. For a detailed analysis, please contact your pension fund or a financial planner.

Lump-sum payout

Regular pension

Lump-sum payment or pension? Determine the intersection point.

Horizontal scale: Life expectancy

Vertical scale: Advantage or disadvantage of pension withdrawals compared to lump-sum withdrawals

The intersection indicates the age at which the pension is financially more advantageous than the lump-sum withdrawal; the figures are based on the assumption that the lump-sum withdrawal takes place at the age of 65 and the pension conversion rate does not fall.

The pension

A pension provides a relatively secure income and enables you to plan your finances. When you retire, the pension assets you have saved up are converted into a lifelong pension that is paid out regularly. The advantage of this pension solution is its stability: regardless of market fluctuations, the pension payments remain constant, thus ensuring a predictable income for the rest of your life.

The amount of your pension depends on the conversion rate of your pension fund. This indicates the percentage of the capital saved that is paid out as a pension each year. A higher conversion rate results in a higher pension, while a lower conversion rate results in a correspondingly lower income.

Conversion rate

The conversion rate indicates the percentage of the retirement capital that is paid out annually as a pension. Although the statutory conversion rate is still 6.8% (as of 2024) following the failure of the last BVG revision, many foundations are already applying significantly lower conversion rates. This is possible because the statutory conversion rate only applies to the mandatory portion of the pension and the foundation is free to set the conversion rate for the non-mandatory portion. In total, this can lead to a conversion rate that is below the legal minimum.

Example: If you have CHF 250'000 in pension assets in your pension fund and the enveloping conversion rate of your pension fund is 5%, you will receive CHF 12'500 per year for life (CHF 250'000 * 5%).

Lump-sum withdrawal

If you withdraw your pension capital as a lump sum, you have to decide whether you want to invest the capital yourself or entrust its management to a bank or asset manager. If you want to manage the capital yourself, it is important that you actually invest it, preferably passively and with a clear strategy. This may sound obvious, but it is not. In practice, many private investors act emotionally and leave substantial sums in their bank accounts, where they earn no return and inflation erodes the value of the money.

To beat inflation, you need a return after costs that is higher than the respective inflation rate. Achieving this is a challenge. If you make mistakes when investing and suffer heavy losses, you run the risk of suddenly having too little money to finance your standard of living in old age.

In short, the goal is to achieve the best possible risk-return ratio.

The most important differences

Regular pension

Income

Lifelong guaranteed, constant nominal income.

Amount of income

Depends on the conversion rate of the pension fund.

Flexibility

Fixed monthly pension.

Taxes

The pension paid out is taxed at 100% as income. This leads to a current tax burden.

Risks

The pension usually remains unchanged and is not adjusted for inflation. This can lead to a loss of purchasing power over the years.

Survivors

The statutory pension for surviving dependants (spouses and surviving registered partners) from the 2nd pillar is 60% of the retirement pension. Unmarried surviving dependants have no statutory entitlement.

Lump-sum payout

Income

Paying out all or part of the pension assets.

Amount of income

Depending on the investment strategy.

Flexibility

Freely plannable capital withdrawals.

Taxes

One-time taxation at the time of payment, separate from other income and generally at a lower rate. Thereafter, the remaining capital is subject to wealth tax and the income derived from it is taxed as income.

Risks

If you live longer than expected or the investment result is worse than assumed, you will have to rely on other sources of income (AHV, relatives, etc.).

Survivors

The assets remain in the possession of the heirs and are subject to the rules of matrimonial property and inheritance law.

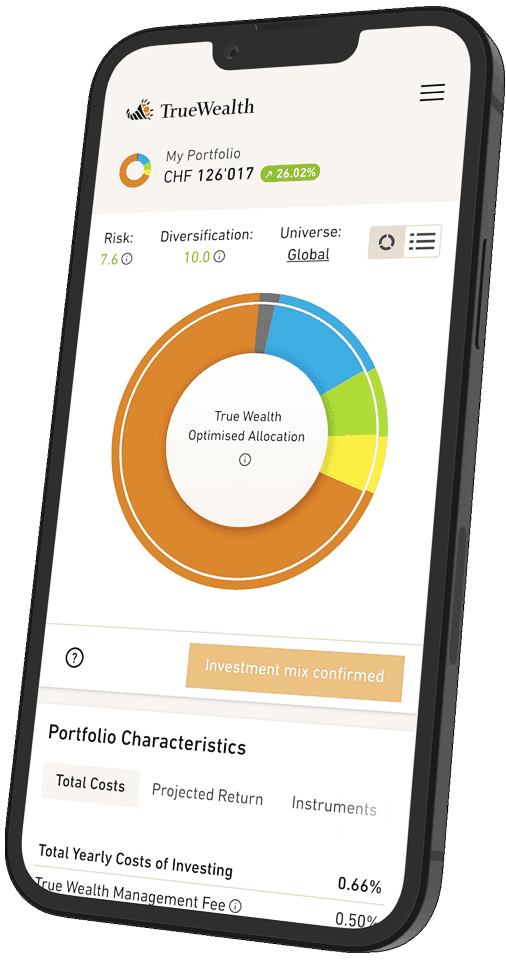

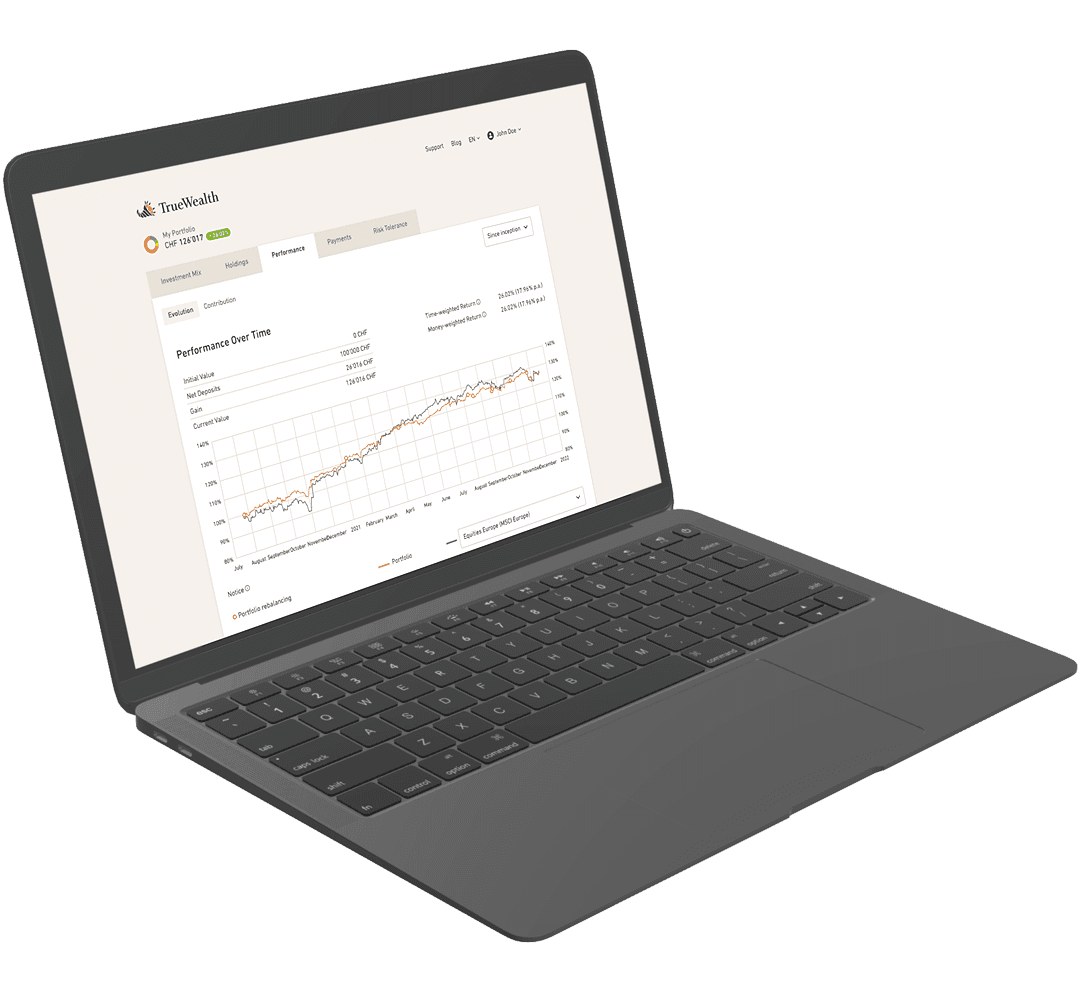

A comfortable retirement with regular payouts

To cover your living expenses after retirement, you will need to make regular withdrawals from your retirement savings.

True Wealth's withdrawal plan allows you to set your withdrawal amounts easily and flexibly. You are in complete control and can adjust your payouts to suit your individual needs and circumstances at any time.

Your advantages with True Wealth

- Low costs and fees

Only 0.25-0.50% wealth management fee per year. - Automatic rebalancing

Portfolios are regularly reviewed and adjusted as necessary to ensure optimal diversification. - High liquidity

You can dispose of your assets at any time. - Individual portfolios

You receive a portfolio tailored to your personal risk profile. This can be adjusted if necessary. - Simple and clear reporting

The online login and the app keep you on top of things. All reports are clear and transparent.

Questions & answers

We are happy to answer any question you may have. You can find the most frequently asked questions right here.

Ready to invest?

Open accountNot sure how to start? Open a test account and upgrade to a full account later.

Open test account